Twenty-three of the 100 largest companies listed on the Bombay Stock Exchange have failed to deliver robust annual returns over the past three years [1].

This trend suggests a widening gap in performance among India's blue-chip stocks, indicating that market leadership does not guarantee investor profit. The underperformance of these giants may signal deeper systemic issues within key sectors of the Indian economy.

According to the Economic Times India, a significant portion of the BSE 100 has struggled to provide meaningful returns [1]. Many of these stocks are currently trading below their historical valuations [1]. This decline is attributed to a combination of cautious client spending and concerns regarding rural demand [1].

Sector-specific challenges have played a primary role in this slump. The Consumer, IT, and Banking, Financial Services and Insurance (BFSI) sectors have been particularly impacted by these economic headwinds [1]. The lack of growth in these areas has weighed down the overall performance of the index's top tier.

Despite these broader struggles, some industry leaders remain optimistic. An analyst said that giants like Reliance Industries Ltd (RIL) and Tata Consultancy Services (TCS) are poised for growth driven by new ventures and expansion [1]. This suggests a divergence where only the most aggressive expanders are overcoming the current economic climate.

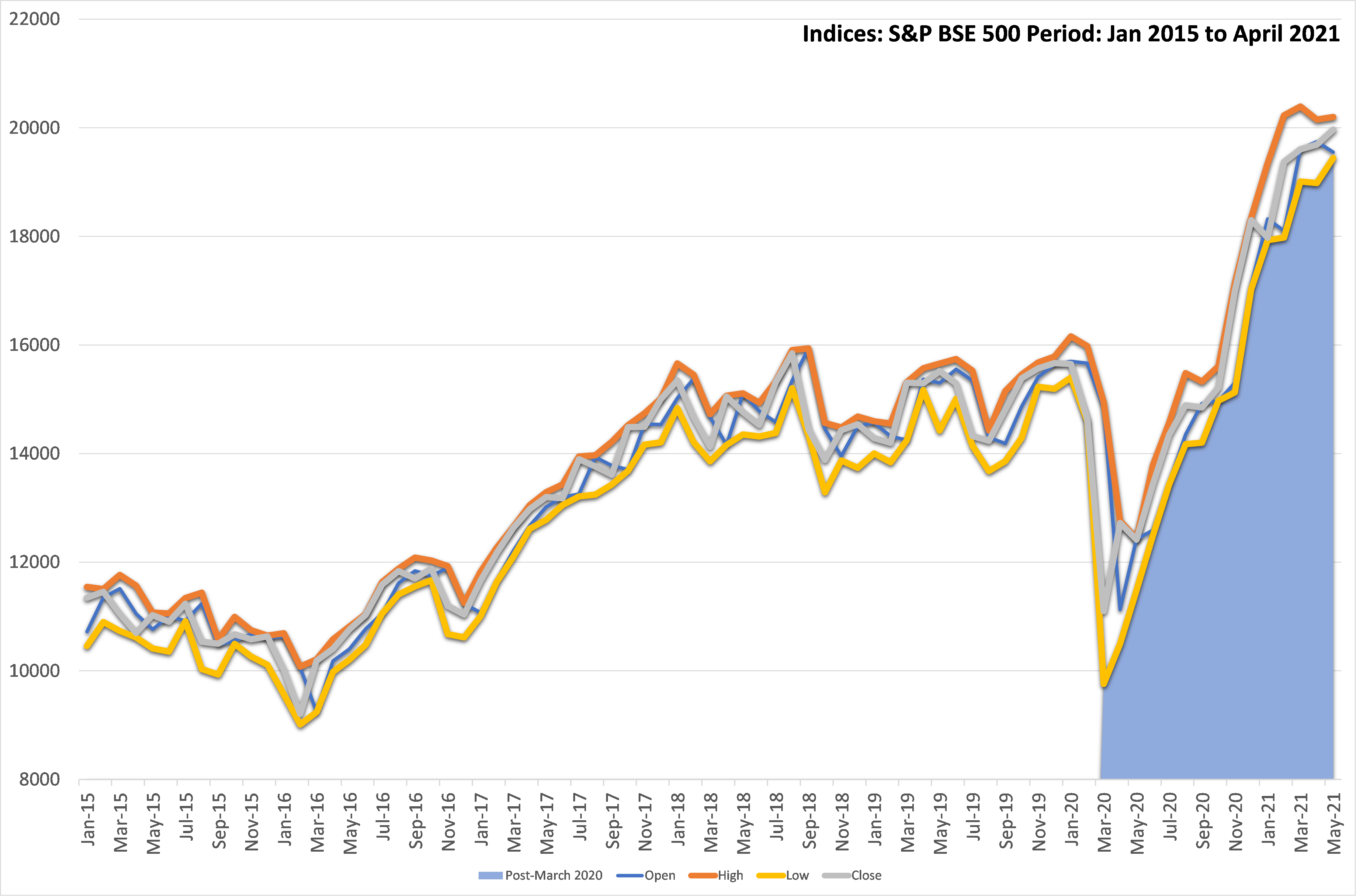

The struggle for these 23 companies comes during a period where the broader market has seen volatility [1]. The fact that nearly a quarter of the top 100 companies are underperforming highlights the volatility inherent in the current fiscal landscape.

“Twenty-three of the 100 largest companies listed on the Bombay Stock Exchange have failed to deliver robust annual returns.”

The underperformance of nearly 25% of the BSE 100 indicates that the 'blue-chip' label is no longer a reliable proxy for stability or growth in the Indian market. With significant declines in IT and BFSI sectors, the data suggests that macroeconomic pressures—specifically rural demand and global client spending—are outweighing the inherent strength of these large-cap entities.