The Indian government implemented modest price hikes for diesel and petrol this month to cushion the economy from soaring global oil prices [1].

These measures aim to protect the rupee and mitigate inflationary pressures caused by the escalation of the Iran-West Asia conflict. The government is attempting to prevent capital outflows as the energy crisis threatens national economic stability [2, 3].

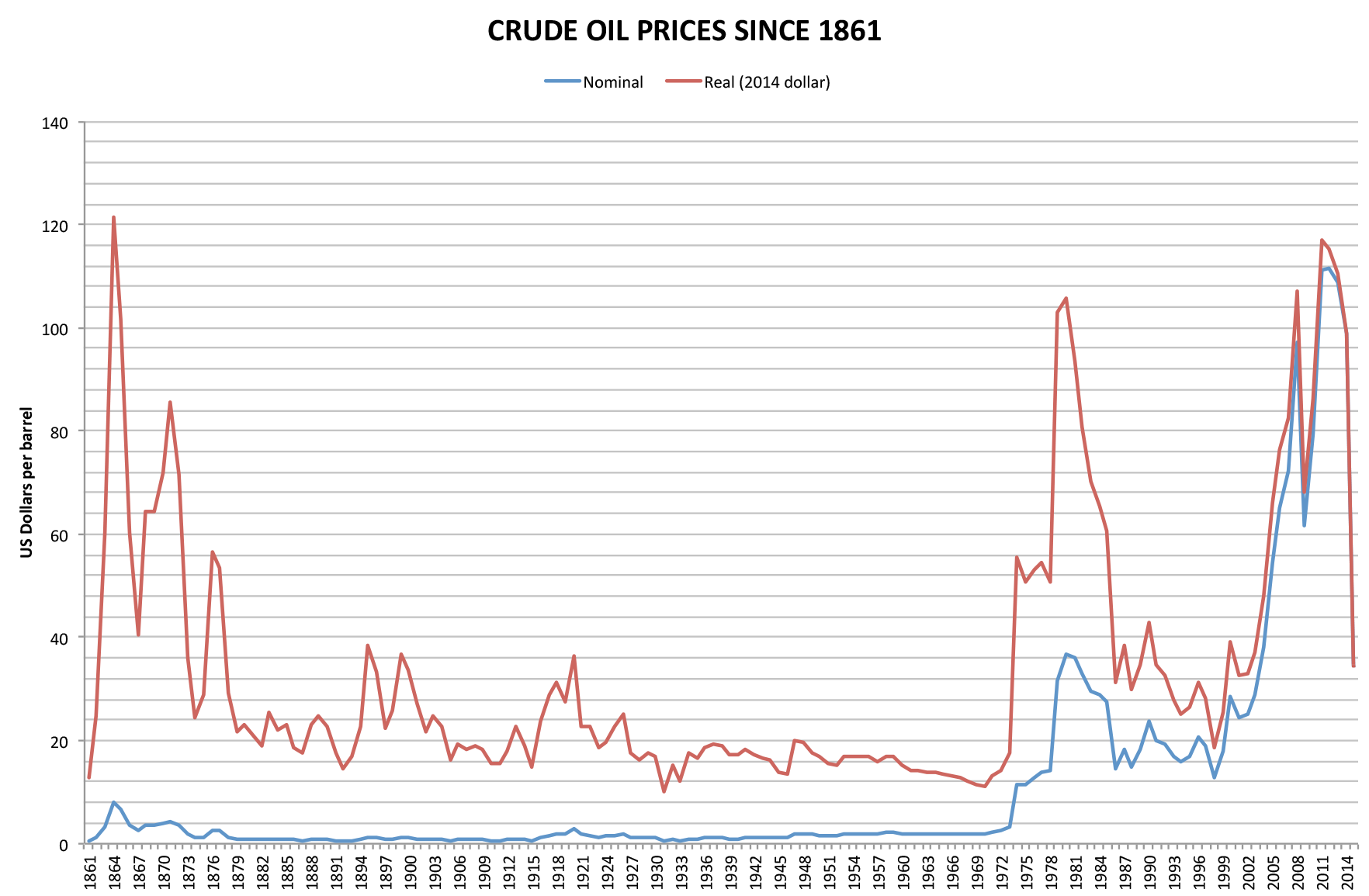

Crude oil prices have crossed $100 per barrel since the start of the Middle East conflict [4]. To address the immediate financial strain, the government increased diesel and petrol prices by more than three percent [1].

The shock to the energy sector is severe. India has lost more than 40% of its crude oil flows since the Hormuz Strait closed [5]. This disruption has left oil marketing companies bleeding approximately 1,000 crore rupees per day [5].

Beyond immediate price adjustments, policymakers are accelerating the procurement of electric buses to reduce long-term dependence on fossil fuels [1, 2]. These fiscal steps are designed to shield the broader economy from the volatility of the global energy market, a necessity given the country's high reliance on imported oil [3].

Government officials said these steps are necessary to maintain macroeconomic stability. By allowing fuel prices to rise slightly, the state reduces the subsidy burden on oil companies, and slows the depletion of foreign exchange reserves [2, 3].

“India has lost over 40% of its crude oil flows since the Hormuz Strait closed”

India's strategy reflects a pivot from total price stabilization to a managed-inflation approach. By accepting modest fuel price hikes and accelerating the transition to electric transit, the government is attempting to decouple its economic growth from the volatility of the Hormuz Strait. The scale of the daily losses for oil companies suggests that without these interventions, the state would face a critical fiscal deficit or a sharp devaluation of the rupee.