Indian equity benchmarks ended lower on May 31, 2026, as selling pressure intensified across the NIFTY 50 and Sensex indices [1, 2, 3].

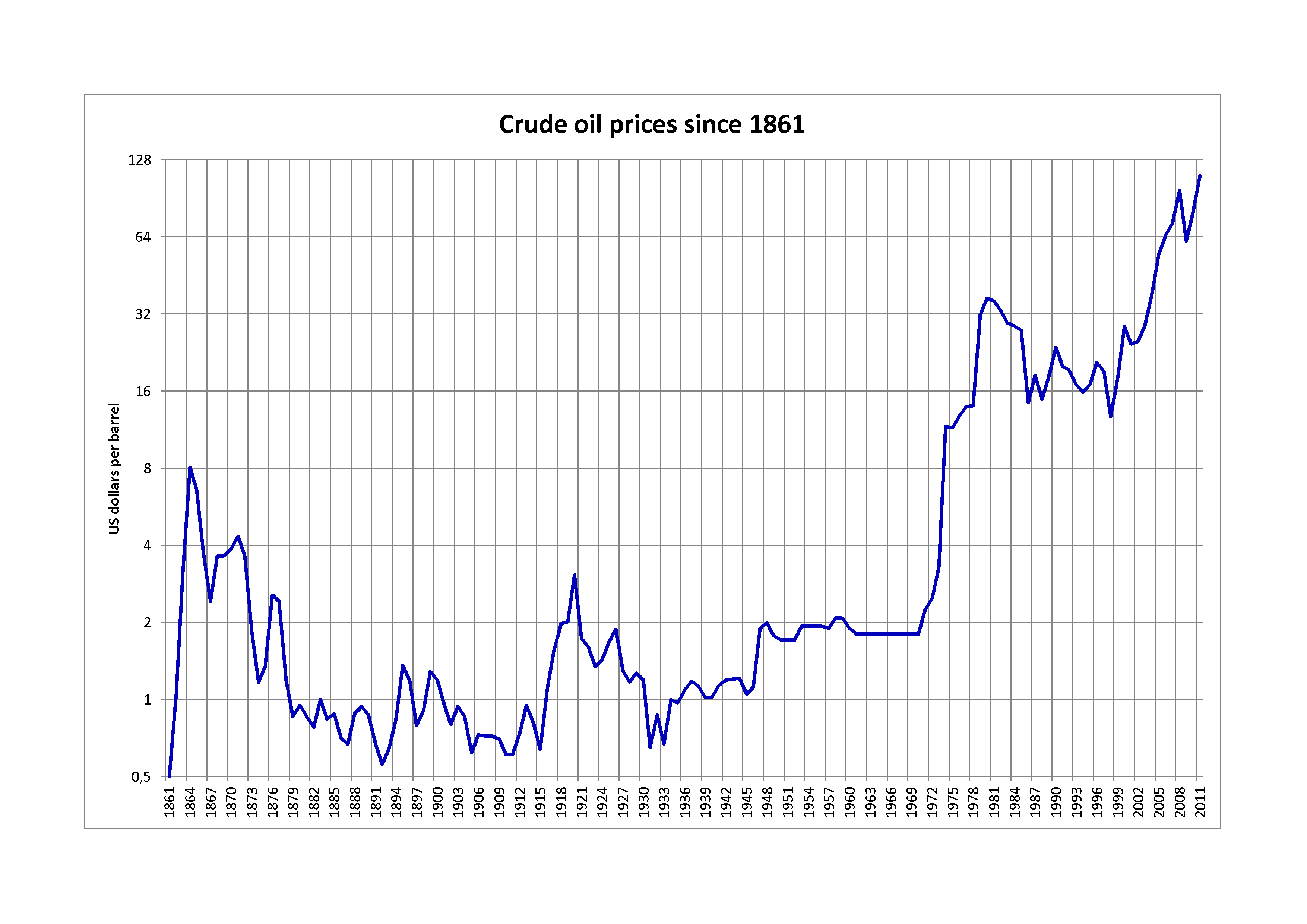

This downturn reflects the vulnerability of India's economy to external shocks, specifically the volatility of energy prices and geopolitical instability in the Middle East.

The NIFTY 50 slipped below 23,600 [1]. Other segments of the market saw similar declines, with the Nifty mid-cap index falling 1.4% and the small-cap index dropping 1% [1]. Reports on the Nifty 50's overall decline varied, with one source citing a drop of 240 points [3].

The Sensex experienced significant volatility during the session. While some reports indicated a decline of 114 points [2], other data showed the index fell by over 800 points [3].

Market analysts said the slump was due to heightened tensions stemming from the U.S.-Iran war and a rally in crude oil prices [1, 3]. India is a major importer of crude oil, meaning price spikes typically increase costs for businesses and fuel inflation.

Some experts said the decline could deepen if the conflict escalates. Projections indicate the NIFTY 50 could potentially slip to 22,000 or even 19,000 depending on the trajectory of the U.S.-Iran war [4].

“NIFTY 50 slipped below 23,600”

The simultaneous drop in mid-cap and small-cap indices alongside benchmark indices suggests a systemic risk-off sentiment among investors. Because India relies heavily on imported oil, the correlation between U.S.-Iran geopolitical tensions and market volatility is direct; rising oil prices act as a tax on economic growth, prompting investors to exit equity positions in anticipation of lower corporate earnings.

'%2F%3E%0A%20%20%20%20%3Crect%20width%3D'1600'%20height%3D'900'%20fill%3D'url(%23v)'%2F%3E%0A%20%20%20%20%3Cg%20opacity%3D'0.08'%20fill%3D'%23ffffff'%3E%0A%20%20%20%20%20%20%3Ccircle%20cx%3D'1420'%20cy%3D'180'%20r%3D'220'%2F%3E%0A%20%20%20%20%20%20%3Ccircle%20cx%3D'1500'%20cy%3D'760'%20r%3D'120'%2F%3E%0A%20%20%20%20%3C%2Fg%3E%0A%20%20%20%20%3Cline%20x1%3D'80'%20y1%3D'172'%20x2%3D'220'%20y2%3D'172'%20stroke%3D'%23ffffff'%20stroke-width%3D'3'%20stroke-opacity%3D'0.6'%2F%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'140'%20font-family%3D'Inter%2C%20-apple-system%2C%20Helvetica%2C%20sans-serif'%20font-weight%3D'700'%20font-size%3D'28'%20fill%3D'%23ffffff'%20letter-spacing%3D'6'%3EHANNA%20%C2%B7%20NEWS%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'230'%20font-family%3D'Inter%2C%20-apple-system%2C%20Helvetica%2C%20sans-serif'%20font-weight%3D'600'%20font-size%3D'40'%20fill%3D'%23ffffffb3'%20letter-spacing%3D'4'%3EBUSINESS%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'622'%20font-family%3D'Playfair%20Display%2C%20Georgia%2C%20serif'%20font-weight%3D'800'%20font-size%3D'86'%20fill%3D'%23ffffff'%20letter-spacing%3D'-1'%3EIndia%20More%20Sensitive%20to%3C%2Ftext%3E%3Ctext%20x%3D'80'%20y%3D'721'%20font-family%3D'Playfair%20Display%2C%20Georgia%2C%20serif'%20font-weight%3D'800'%20font-size%3D'86'%20fill%3D'%23ffffff'%20letter-spacing%3D'-1'%3ECrude%20Oil%20Prices%20Than%20EM%3C%2Ftext%3E%3Ctext%20x%3D'80'%20y%3D'820'%20font-family%3D'Playfair%20Display%2C%20Georgia%2C%20serif'%20font-weight%3D'800'%20font-size%3D'86'%20fill%3D'%23ffffff'%20letter-spacing%3D'-1'%3EPeers%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'870'%20font-family%3D'Inter%2C%20-apple-system%2C%20Helvetica%2C%20sans-serif'%20font-weight%3D'500'%20font-size%3D'22'%20fill%3D'%23ffffff66'%20letter-spacing%3D'2'%3Enews.hanna-ai.com%3C%2Ftext%3E%0A%20%20%3C%2Fsvg%3E)