Oil prices reached wartime highs on Thursday as President Donald Trump weighed military options to end the war with Iran [1].

The surge threatens global economic stability and increases costs for consumers at the pump as the blockade of the Strait of Hormuz continues [1, 2].

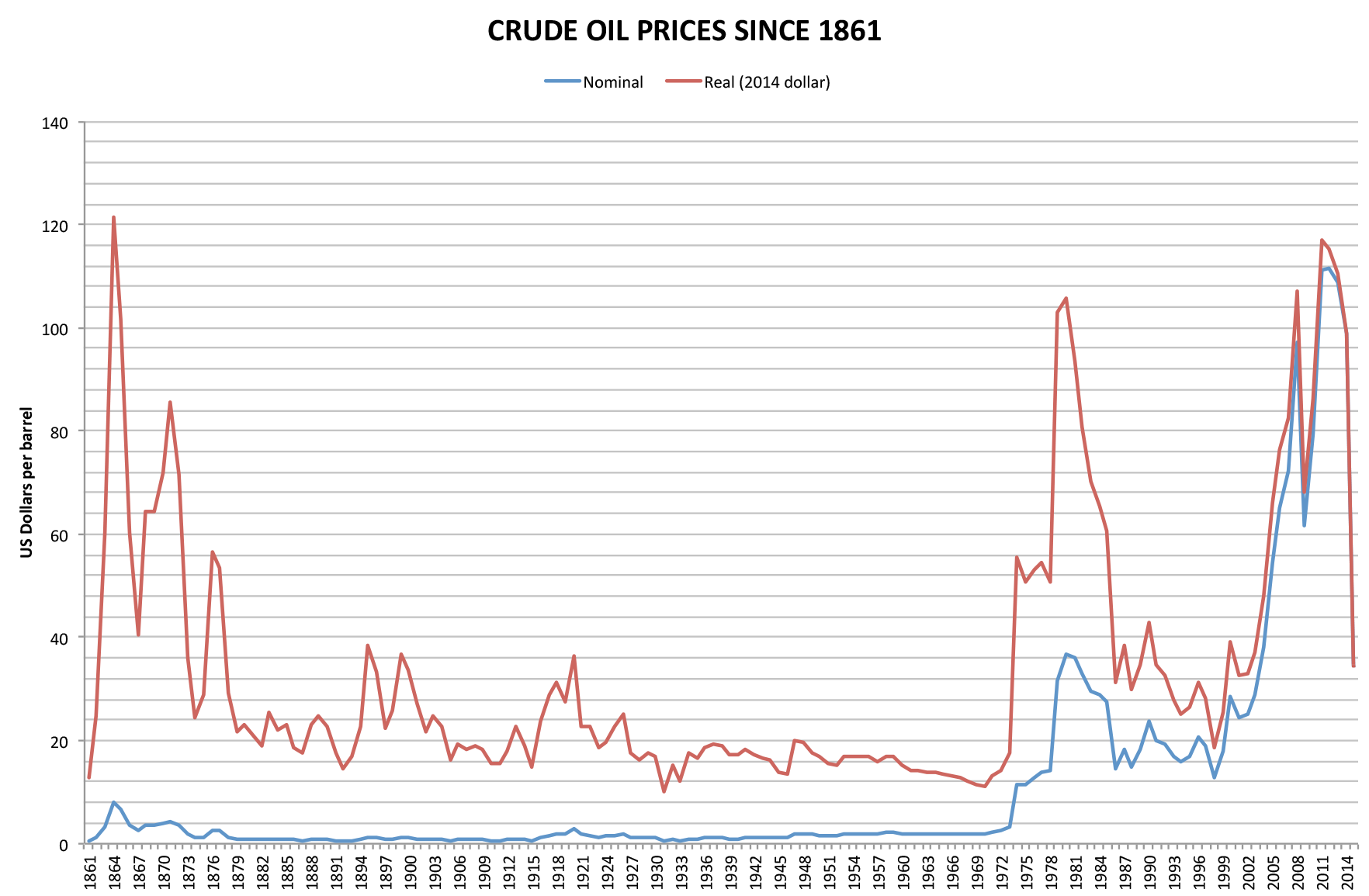

Brent crude briefly surged past $126 a barrel early Thursday [1]. Other reports indicated price levels around $116 per barrel [3]. The volatility follows stalled peace negotiations between the U.S. and Iran, and a continuing blockade of the Persian Gulf [1, 2].

President Trump said, "I could live with not taking over the Strait of Hormuz" [4]. Despite this statement, the president has been briefed on potential military options to resolve the conflict [5].

In Washington, U.S. Defense Secretary Lloyd Hegseth faced questioning from lawmakers regarding the administration's strategy in the region [1]. The military presence in the Middle East has increased, with 3,500 additional U.S. troops deployed [3].

Reports on the origins of the conflict vary. Some sources attribute the war to a joint U.S. and Israeli operation that assassinated supreme leader Ayatollah Ali Khamenei four weeks ago [6]. Other reports link the current escalation to the failed diplomatic talks and the maritime blockade [1].

The Associated Press said, "Consumers are already feeling the effects of the war and its destabilizing effect on worldwide energy" [7].

“"Brent crude briefly surged past $126 a barrel early Thursday."”

The convergence of record-high energy prices and military escalation in the Persian Gulf creates a precarious economic environment. With the Strait of Hormuz—a critical chokepoint for global oil transit—under blockade, the U.S. faces a dilemma between escalating military intervention to secure energy flows or risking prolonged economic volatility through stalled diplomacy.

'%2F%3E%0A%20%20%20%20%3Crect%20width%3D'1600'%20height%3D'900'%20fill%3D'url(%23v)'%2F%3E%0A%20%20%20%20%3Cg%20opacity%3D'0.08'%20fill%3D'%23ffffff'%3E%0A%20%20%20%20%20%20%3Ccircle%20cx%3D'1420'%20cy%3D'180'%20r%3D'220'%2F%3E%0A%20%20%20%20%20%20%3Ccircle%20cx%3D'1500'%20cy%3D'760'%20r%3D'120'%2F%3E%0A%20%20%20%20%3C%2Fg%3E%0A%20%20%20%20%3Cline%20x1%3D'80'%20y1%3D'172'%20x2%3D'220'%20y2%3D'172'%20stroke%3D'%23ffffff'%20stroke-width%3D'3'%20stroke-opacity%3D'0.6'%2F%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'140'%20font-family%3D'Inter%2C%20-apple-system%2C%20Helvetica%2C%20sans-serif'%20font-weight%3D'700'%20font-size%3D'28'%20fill%3D'%23ffffff'%20letter-spacing%3D'6'%3EHANNA%20%C2%B7%20NEWS%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'230'%20font-family%3D'Inter%2C%20-apple-system%2C%20Helvetica%2C%20sans-serif'%20font-weight%3D'600'%20font-size%3D'40'%20fill%3D'%23ffffffb3'%20letter-spacing%3D'4'%3EWORLD%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'694'%20font-family%3D'Playfair%20Display%2C%20Georgia%2C%20serif'%20font-weight%3D'800'%20font-size%3D'110'%20fill%3D'%23ffffff'%20letter-spacing%3D'-1'%3EVenezuela%20Earthquake%20Death%3C%2Ftext%3E%3Ctext%20x%3D'80'%20y%3D'820'%20font-family%3D'Playfair%20Display%2C%20Georgia%2C%20serif'%20font-weight%3D'800'%20font-size%3D'110'%20fill%3D'%23ffffff'%20letter-spacing%3D'-1'%3EToll%20Rises%20to%202%2C295%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D'80'%20y%3D'870'%20font-family%3D'Inter%2C%20-apple-system%2C%20Helvetica%2C%20sans-serif'%20font-weight%3D'500'%20font-size%3D'22'%20fill%3D'%23ffffff66'%20letter-spacing%3D'2'%3Enews.hanna-ai.com%3C%2Ftext%3E%0A%20%20%3C%2Fsvg%3E)