Brent crude prices fell by $18 in May [1], marking the sharpest dollar-term drop for the commodity since the early stages of the Covid-19 pandemic [1].

This volatility reflects a shifting geopolitical landscape and a pivot in investor behavior, where energy instability is driving a flight toward the perceived safety of utility stocks.

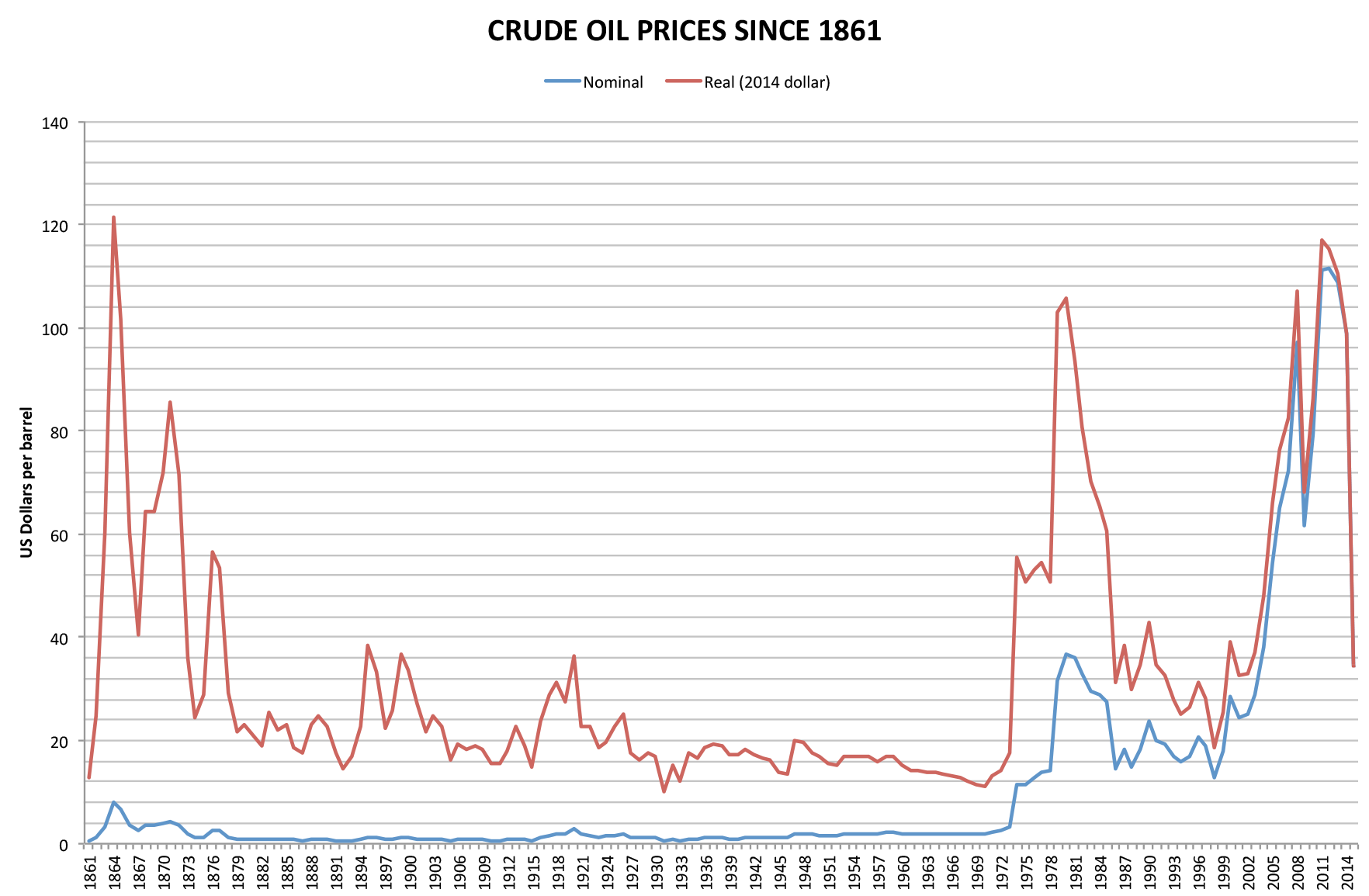

Market analysts said that May was the worst month for oil prices since 2020 [2]. This decline was driven largely by hopes surrounding Trump-related negotiations involving Iran and the Strait of Hormuz [2]. Earlier in the spring, optimism over U.S.-Iran negotiations and a 10-day cease-fire between Israel and Lebanon also contributed to downward pressure on oil [3].

While oil struggled, the utilities sector saw a surge in interest. Traders rotated into utility stocks as safe-haven assets ahead of a three-day weekend [4]. This trend benefited companies including American Water Works, and Essential Utilities [5].

In the broader energy sector, the U.S. energy-storage industry reported a significant milestone. The industry installed a record amount of capacity during the first quarter of 2026 [4]. This expansion is intended to improve overall grid stability as power producers integrate more variable energy sources.

Other company updates in the sector included movements involving Seatrium and various power producers [5]. The combination of record storage growth and fluctuating fuel prices suggests a transition period for the U.S. energy infrastructure as it balances traditional commodities with new technology [4], [5].

“May was the worst month for oil prices since 2020”

The divergence between plummeting oil prices and rising utility stocks indicates a market hedging against geopolitical instability. While diplomatic hopes are lowering the cost of crude, the record installation of energy-storage capacity suggests a long-term strategic shift toward grid resilience and a reduction in reliance on volatile fossil fuel markets.